Types of Bankruptcies

There are different chapters for different bankruptcies under the U.S. Bankruptcy Code; however, the most common types and relevant for valuation include Chapter 7 (Liquidation) and Chapter 11 (Reorganization).

In Chapter 7, the debtor’s estate is liquidated under the rules under which the debtor’s non-exempt property is liquidated in an orderly transaction by a trustee and the cash proceeds are distributed to the creditors.

Chapter 11 allows the debtor to reorganize without having to liquidate all assets. The debtor presents a reorganization plan which, if accepted by the creditors and approved by the Bankruptcy Court, will allow the debtor to reorganize affairs and continue operations. The filing of a bankruptcy petition creates an estate, and the debtor’s property becomes the property of the estate. The debtor is permitted to retain and use this property as the debtor in possession (“DIP”) subject to the need to provide adequate protection for the creditor’s security interest in the property.

[1] The Small Business Reorganization Act of 2019 added a new subchapter V to Chapter 11, designed to make bankruptcy easier for small businesses (which are defined as entities with less than about $2.7 million in debts that also meet other criteria).[2] The Coronavirus Aid, Relief, and Economic Security (“CARES”) Act, signed into law on March 27, 2020, raised the Subchapter V debt limit to $7.5 million. The change applies to bankruptcies filed after the CARES Act was enacted.[3] Pursuant to the COVID-19 Bankruptcy Relief Extension Act signed on March 27, 2021, the debt limit of $7.5 million is now extended to March 27, 2022, which was earlier expected to expire on March 27, 2021.[4]

Purpose of Valuation

Bankruptcy courts determine value on a case-by-case basis keeping in view facts and circumstances surrounding the subject company. The situations where bankruptcy valuation comes into effect include DIP financing collateral determination, adequate protection for creditors, claims determination, asset recovery (including preferences, fraudulent transfers, and reclamation), reorganization plan confirmation, determination of liquidation values and valuation of intangible assets in a bankruptcy, and implementing post-Chapter 11 bankruptcy fresh-start accounting. A valuation prepared for one purpose may not be applicable for another purpose. Hence, it is important for the valuation analyst to understand and document the purpose of the valuation.[5]

Standard of Value

Bankruptcy courts determine value on a case-by-case basis keeping in view facts and circumstances surrounding the subject company. The situations where bankruptcy valuation comes into effect include DIP financing collateral determination, adequate protection for creditors, claims determination, asset recovery (including preferences, fraudulent transfers, and reclamation), reorganization plan confirmation, determination of liquidation values and valuation of intangible assets in a bankruptcy, and implementing post-Chapter 11 bankruptcy fresh-start accounting. A valuation prepared for one purpose may not be applicable for another purpose. Hence, it is important for the valuation analyst to understand and document the purpose of the valuation.[6]

Premise of Value

[7]The main premise of value applicable to business valuation are going concern value and liquidation value. In bankruptcy valuations, care should be taken to ensure that the highest and best use is reasonably available to the debtor and property in question. In Chapter 7 bankruptcy, the required premise is liquidation, and orderly liquidation value is typically used. In certain cases, the premise of value is not clear and may require consideration of court precedent and the actual operating characteristics of the company, as well as the intended use of the property. In Chapter 11 bankruptcy, courts often require the use of going concern value unless evidence indicates that the business is on a “deathbed”.

Bankruptcy Tests

Solvency Tests

In the context of bankruptcy, most actions taken to recover assets involve a determination that the debtor was insolvent at the time of transfer (Constructive Fraud scenario). To determine this, the valuation of selected assets of the business is required, and solvency tests are performed.[8] The test for insolvency in a bankruptcy proceeding is similar to the process undertaken for issuing a solvency opinion with respect to a contemporaneous transaction. Under either scenario, if the company fails any of three tests, it is considered insolvent.[9]

- Balance sheet test: If the market value of the company’s assets exceeds the value of its liabilities, the balance sheet test is passed. Enterprise value should be greater than the net assets of the company to be considered solvent. The market value of assets that generally may not be listed on the balance sheet, such as intangible assets, should be included. Debts include estimates of contingent or unliquidated liabilities;

- Cash flow test: This test measures a company’s ability to generate cash flows to pay its debts as they mature. It measures a company’s ability to pay its bills as of a specific date and is concerned primarily with equity for the protection of creditors. Typically, the projections that are used to value the company under the balance sheet test are reviewed to ensure that the cash flows will be adequate to cover future principal and interest payments on the company’s post-emergence debt after meeting the standard cash flow items such as capital expenditures and increases in working capital; and

Capital adequacy test: This is also known as an unreasonably small capital test and is considered as a stress test of cash flow projections. This test includes a stress test of the proposed plan, assessing how sensitive the feasibility of the plan is to small changes in underlying assumptions. Essentially, the purpose of this test is to measure the “margin of error” in the underlying projections.

Best Interests of Creditors Test

The best interests test must be met to approve the reorganization plan under Chapter 11. The best interests test requires that each creditor of the company receive under that plan at least as much as it would receive in a liquidation under Chapter 7 of the Bankruptcy Code.[10] Bankruptcy Code § 1129(a)(7) states that:[11] With respect to each impaired class of claims or interests – (A) each holder of a claim or interest of such class … (ii) will receive or retain under the plan on account of such claim or interest property of a value, as of the effective date of the plan, that is not less than the amount that such holder would so receive or retain if the debtor were liquidated under chapter 7 of this title on such date.

Solvency Opinions

Solvency opinion is an opinion on whether a company can meet its debt obligations as they come due. Solvency opinions are used to assess fraudulent conveyance or improper dividend risk. It can also be used to establish fiduciary duty defense for corporate officers and directors. However, it is not a recommendation on whether to pursue a transaction, neither is it a guarantee of financial protection. The solvency is generally determined using the three solvency tests as described above. The solvency opinions are typically sought for the following purposes:

- Transactions, including spin-off and split-off, payment of dividend or distributions, repurchase or redemption of securities, mergers & acquisitions, refinancing, or leveraged recapitalization; and

- Litigation related to Fraudulent Conveyance, which may be related to the transactions noted above.

Valuation Approaches

The primary approaches to valuation: (a) the market; (b) the income; and (c) the asset-based (cost) is considered in bankruptcy engagements when the premise is going concern value. Even in the case of liquidation, these approaches are applicable when valuing individual assets or a group of assets.

The precursor to any bankruptcy is financial distress. Many companies in the manufacturing, energy, retail, aviation, hotel sectors were hardly hit by COVID-19, which pushed them into bankruptcy.

Market Approach

This approach can be applied by (i) using a set of distressed guideline public companies, which may be difficult to identify. This is generally because the likely guideline public companies (“GPCs”) may not be in the same distressed financial condition as the subject company; or (ii) adjusting the GPC’s multiple for distress, which will be applied to the subject company’s metrics such as revenue or earnings before interest, taxes, depreciation, and amortization (“EBITDA”). The subject company’s revenue and earnings may not be meaningful metrics, and normalized operating indicators should be used to value the subject company. Further, the subject company may not have meaningful historical earnings to which the comparable multiples may be applied. In that case, either the revenue multiples may be applied, forward earnings multiples of the GPCs can be used, or the historical earnings multiples can be applied to the forward revenue of the subject company, and this value can be discounted to present value.[13] This approach is similar to valuing early-stage companies or companies that are yet to achieve meaningful profitability levels.

Income Approach

[14],[15]The expected cash flows and discount rate should be adjusted to reflect the likelihood of distress. The probability distribution for the inputs into DCF valuation, such as revenue growth, EBITDA margin, can be applied, and simulation can be run to capture a set of negative cash flow outcomes eventually leading to distress. For an estimate of terminal value, the exit multiples may be used; however, these may need to be discounted for risks. The beta used to estimate the cost of equity can be estimated using the debt and equity ratio based on the financial and operating risks faced by the subject company. Further, the cost of debt can be increased to reflect the default risk of the subject company. The use of venture capital rates of return may be appropriate for certain high-risk but potentially high return situations.

Cost Approach

The basic theory behind the asset-based approach is current value of assets minus current value of liabilities equals the current value of the Company.[16] In case of bankruptcy, the asset-based approach can be applied with various standards of value and with various premises of value. The debtor company net book value is not a meaningful variable in the asset-based approach analysis. This analysis should encompass the valuation of all debtor company asset accounts: current assets, real estate, tangible personal property, intangible personal property and unconsolidated investments and other assets.[17]

Valuation Considerations for Bankrupt Entities

[18],[19]The analyst has to make many decisions when valuing a distressed company (whether or not the company has filed for bankruptcy). The analyst needs to perform adequate due diligence of management-provided projections. The analyst needs to decide whether the valuation variables should reflect the current state of the debtor or the reorganized state of the debtor in the bankruptcy setting. The analyst may also consider how the assumed financial condition of the debtor company affects its cost of debt, its cost of equity, its capital structure, and its weighted average cost of capital (“WACC”). If the analyst assumes a reorganized debtor company, the analysis may incorporate a different discount rate than the one appropriate for a financially troubled company and also consider different operating and capital expenditures.

Additionally, the analyst should consider the debtor company’s expected use of any net operating loss (“NOL”) tax attributes. In a bankruptcy, it is common for a creditor to forgive some of the debtor’s long-term debt. Such debt forgiveness may cause the debtor company to recognize the cancellation of debt income (“COD”) under the Internal Revenue Code (“IRC”). The debtor may be able to avoid COD income if it is in Chapter 11 bankruptcy protection; however, this exemption will cause the debtor company to lose the benefit of certain tax attributes, such as NOLs. Further, there may be a change of ownership due to the reorganization, which may limit the use of NOLs subject to IRC Section 382.

Recent Trends in Bankruptcy

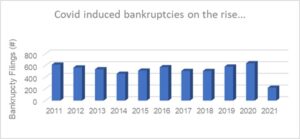

The U.S. economy had a tumultuous year in 2020 due to COVID-19, which triggered a wave of bankruptcies. Edward Altman (of the Altman Z-Score) predicted a large number of corporate bankruptcies in 2020 due to economic conditions and rising corporate debt.[20] The prediction has come true as statistics indicate 639 U.S. public and private companies filing for bankruptcy in 2020, which has significantly increased from a five-year low of 507 in 2018. We note bankruptcies filings year-to-date for period ended May 31, 2021 stood at 219, reflecting improvement in business environment with vaccination picking pace.

Source: CapitalIQ

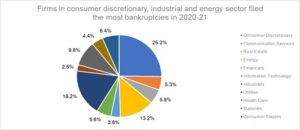

Some industries were severely impacted by the economic downturn due to COVID-19. The consumer discretionary sector registered the largest number of bankruptcies as consumers pared back sharply on discretionary spending. Hotels, restaurants, brick-and-mortar retailers, and movie theatres faced a double whammy of declining revenue due to halted operations and huge debt obligations. The fate of the industrial sector is also closely tied to the health of the economy. The industrial sector also suffered amid a grim economic outlook. Industries such as construction, engineering, aviation, and defense saw a decline in business due to lower business spending and investment. The plunge in oil price deteriorated the conditions for the energy sector, which was in a downturn before the onset of the pandemic. The companies, which took large debt financing for expansion projects, were forced to file for bankruptcy as dwindling revenue and inability to service debt caught them between a rock and a hard place. The health care sector also faced challenges due to an increase in costs for treating a larger number of COVID-19 patients, a slowdown in non-emergent care due to shutdown, and treating a larger number of uninsured patients.

Source: CapitalIQ

[1] NY Times, https://www.nytimes.com/2020/06/18/business/corporate-bankruptcy-coronavirus.html.

Emerging from Bankruptcy: Fresh Start Accounting [21]

About the Contributor:

Vivek Shah

Associate Vice President